Outdated loan operations are slowing growth for direct lenders. Trevor Cook, head of product strategy and end-to-end delivery for Carta Loan Operations, explains how some private credit firms are modernising to meet rising complexity and market stress.

Over the past decade, the direct lending industry has experienced sustained and impressive growth. Despite headwinds like rising interest rates, inflation, and ongoing geopolitical uncertainty, private credit has continued to draw significant investor capital.

But beneath these headline figures lies a growing vulnerability: outdated loan operations. While investors and fund managers often focus on underwriting and capital deployment, the systems and workflows supporting loan administration are increasingly under strain.

A complex landscape meets aging infrastructure

The macroeconomic backdrop for private credit has become significantly more challenging in 2025.

Lenders and borrowers alike are grappling with shifting cost structures and tighter capital markets. Earlier this year, the leveraged loan market experienced one of its most volatile periods since the pandemic, with secondary market prices sliding and institutional loan issuance stalling.

Amid these pressures, borrowers are struggling to maintain stable cash flows. Amendments, restructurings, and payment-in-kind (PIK) elections were once used sparingly; now, they are commonplace.

While these flexible deal terms have mitigated defaults and allowed lenders to support borrowers through temporary stress, they have dramatically increased the complexity of loan administration. Each amendment can alter payment schedules, interest rates, waterfall structures, and covenant terms. PIK interest might ease short-term cash burdens for borrowers, but it also adds layers of accounting and reporting complexity.

Operational inefficiency becomes portfolio risk

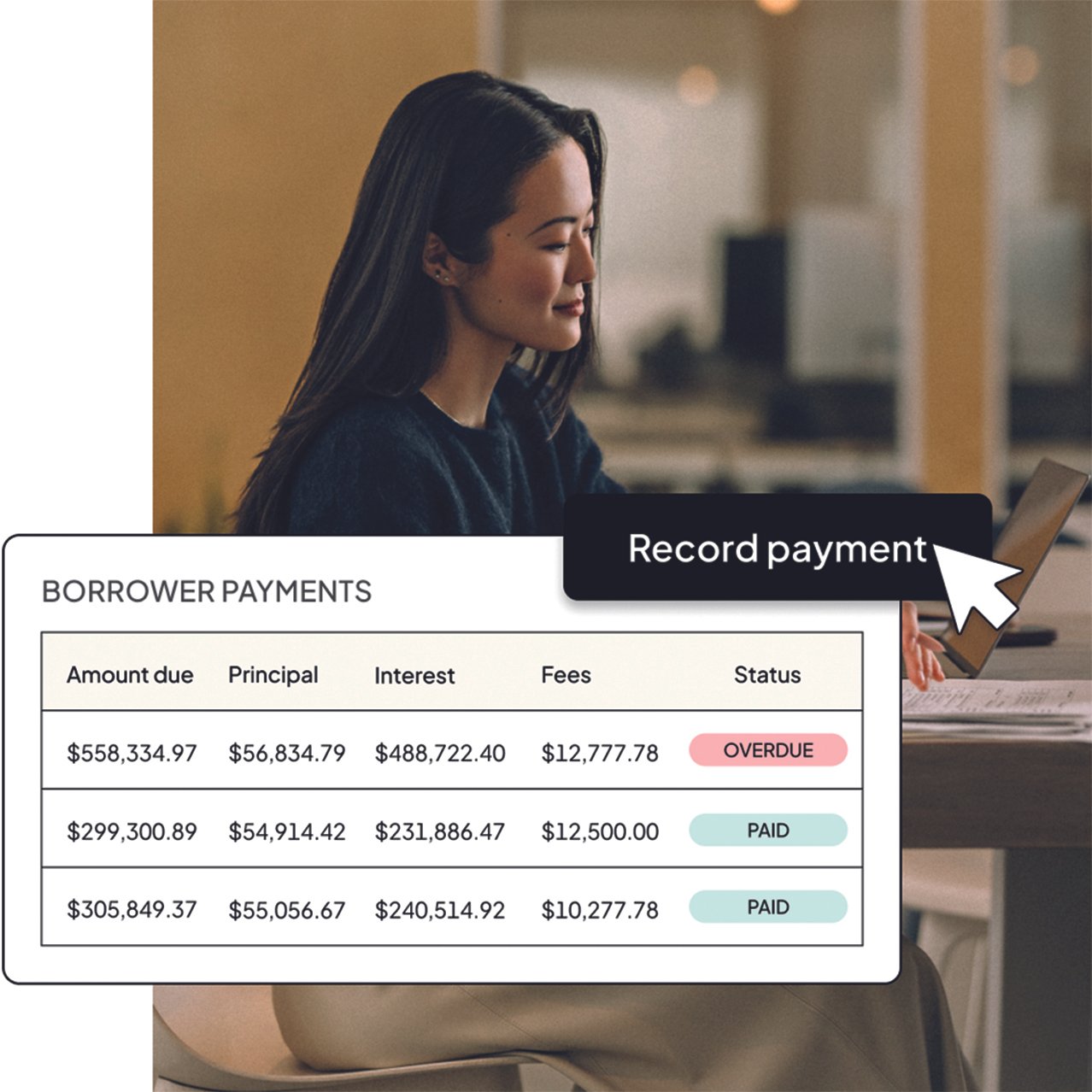

Most loan operations teams still rely on manual workflows built on Excel or legacy software that is ill-equipped to handle today’s dynamic deal structures.

These operational weaknesses are becoming more than just administrative headaches. Indeed, fund managers are postponing defaults and markdowns because their infrastructure cannot keep up with deal complexity and the velocity of change. In some portfolios, this has led to overstated valuations and misreported returns.

While private credit investment teams have embraced data-driven decision-making, the technology supporting loan operations has not kept up. As deals evolve – whether through amendments, restructurings, or pricing changes – updates must often be entered manually across disconnected systems. Reporting typically involves consolidating data from multiple sources, which increases both the workload and the potential for human error.

An inflection point

The private credit industry stands at a critical juncture. Operational workflows that were sufficient five years ago now represent a significant risk.

As investor expectations rise and regulators increase their scrutiny of private credit, the cost of operational shortcomings will only grow. Forward-thinking firms are investing in integrated loan operations technology to automate administrative tasks and manage complex deal structures.

Beyond a desire for greater efficiency, this shift is about enabling scalability, improving accuracy, reducing risk, and ultimately safeguarding both fund performance and investor confidence in a more unpredictable and competitive market.

This is promoted content published in partnership with Carta.