he Internal Revenue Service released its inflation-adjusted Health Savings Account (HSA) limits for 2027, giving Americans with high-deductible health plans additional room to save for current and future healthcare expenses.

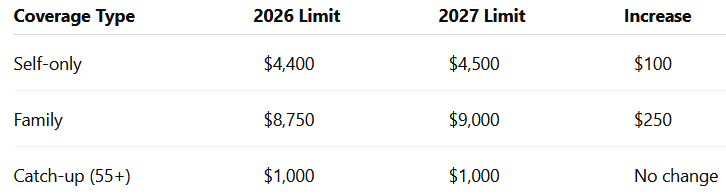

For 2027, individuals with self-only high-deductible health plan (HDHP) coverage will be able to contribute up to $4,500 to an HSA, an increase of $100 from the 2026 limit of $4,400. Those with family coverage can contribute up to $9,000, up $250 from the current $8,750 limit. The additional catch-up contribution for individuals age 55 and older remains unchanged at $1,000.

SEE ALSO: Why a Health Savings Account Can Be Valuable for Federal Employees & Retirees

2027 HSA Contribution Limits

The IRS also increased the thresholds that determine whether a health plan qualifies as an HDHP. Beginning in 2027, the minimum deductible will rise to $1,750 for self-only coverage and $3,500 for family coverage. Meanwhile, maximum annual out-of-pocket expenses will increase to $8,700 for self-only coverage and $17,400 for family coverage.

While the annual increases may appear modest, they can have a meaningful impact over time. HSAs remain one of the few accounts offering a “triple tax advantage:

- contributions are generally tax-deductible,

- investment earnings grow tax-free, and

- withdrawals for qualified medical expenses are tax-free. Financial planners increasingly view HSAs not only as healthcare spending accounts but also as long-term retirement planning tools.

HSA Catch-Up Contributions

For 2027, the HSA catch-up contribution remains $1,000 for individuals who are age 55 or older by the end of the tax year. The catch-up amount is in addition to the regular HSA contribution limit and did not increase because it is set by statute rather than indexed for inflation.

Advertisement

2027 HSA Limits Including Catch-Up Contributions

- If both spouses are age 55 or older, each spouse may make a separate $1,000 catch-up contribution, but each catch-up amount must be deposited into that spouse’s own HSA.

- The catch-up contribution has been $1,000 for many years and is not adjusted annually for inflation.

Spousal HSA catch-up contributions

If you and your spouse are both age 55 or over, not enrolled in Medicare, and otherwise eligible, you each can make $1,000 HSA catch-up contributions, but you must do so in separate HSAs. These contributions can be taken as a tax deduction on your personal taxes assuming they’re not done through payroll deductions.

HSA Rules for Married People

The IRS rules for married people apply only if both spouses are eligible individuals. If either spouse has family HDHP coverage, the family contribution limit applies; both spouses are treated as having family HDHP coverage.

If both spouses are 55 or older and not enrolled in Medicare:

- Each spouse is entitled to increase his or her contribution limit with an additional contribution.

- Their maximum total contributions under family HDHP coverage would include a catch-up contribution for each spouse.

- The contribution limit is divided between the spouses by agreement. If there is no agreement, the contribution limit is split equally between the spouses.

- Any additional contribution for age 55 or over must be made by each spouse to his or her own HSA.

Eligibility to Contribute to an HSA

To be eligible to contribute to an HSA, a participant must be enrolled in an HSA-qualified high deductible health insurance plan (HDHP). Each year the IRS defines what constitutes an HDHP.

A high deductible health plan is defined as a health plan with an annual deductible that is not less than $1,650 for self-only coverage or $3,300 for family coverage, and for which “the annual out-of-pocket expenses (deductibles, co-payments, and other amounts, but not premiums) do not exceed $8,300 for self-only coverage or $16,600 for family coverage,” according to the IRS.

The following information is from OPM regarding HSAs and Federal Employees Health Benefits (FEHB) enrollment:

A Health Savings Account allows individuals to pay for current health expenses and save for future qualified medical expenses on a pre-tax basis. Funds deposited into an HSA are not taxed, the balance in the HSA and interest grows tax free, and that amount is available on a tax free basis to pay your qualified medical expenses, including your copays, coinsurance and deductible.

When you enroll in an HDHP, the health plan determines whether you are eligible for a Health Savings Account (HSA) or a Health Reimbursement Arrangement (HRA) based on the information you provide.

Who is eligible for an HSA?

You are eligible for an HSA if you are:

• Enrolled in an HDHP and not covered by another health plan (including a spouse’s health plan, but not including specific injury insurance and accident, disability, dental care, vision care, or long-term care coverage)

• Not enrolled in Medicare

• Not in receipt of VA or Indian Health Service (IHS) medical benefits within the last three months

The FEHB program offers many types of health insurance plans, including health plans that are HDHP qualified and associated with an HSA. Employees who are currently not enrolled in an FEHB program HDHP and who are interested in enrolling in such a plan associated with an HSA for 2025 may do so during the next FEHB open season to be held from early November 2024 to early December 2024.