Hundreds of thousands of federal employees have left service or will be leaving federal service in the coming months. Many of these employees were or are not eligible to immediately retire from federal service but were eligible for deferred retirement in which they will receive their CSRS or FERS annuities at a later date. They also owned Thrift Savings Plan (TSP) accounts. This column discusses what departed federal employees can do with their TSP accounts.

A departed employee with TSP accounts (traditional TSP and Roth TSP) can keep their accounts with the TSP even though they are no longer in federal service. No withdrawals have to be made from a traditional TSP account until the departed employee reaches their required beginning date (RBD) which is currently April 1 following the year the departed employee becomes 73. At that time and every year thereafter, a Required Minimum Distribution (RMD) must be made from the departed employee’s traditional TSP account.

Contributions to a TSP Account

Upon leaving federal service, a TSP participant is not eligible to make any direct contributions to the TSP to the traditional TSP account and to the Roth TSP account. This is because all direct contributions to the TSP are made via payroll deduction. A federal employee who leaves federal service is no longer receiving a paycheck from a federal agency. In addition, a FERS TSP participant therefore will not receive any agency contributions, including the Agency Automatic (1 percent contribution) and Agency Matching Contributions on their own TSP contributions.

Moving Money into a TSP Account

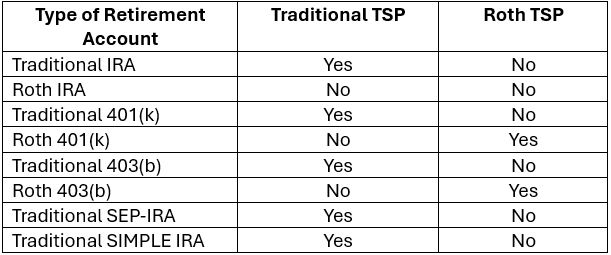

While a departed TSP participant cannot make any direct contributions to their TSP account, a departed TSP participant can make indirect contributions to their TSP accounts via direct rollovers from traditional IRAs and eligible retirement plans. The following table summarizes what can be directly rolled over to the TSP accounts:

Types of retirement accounts that can be directly rolled into a TSP account

TSP Loans Upon Leaving Federal Service

New TSP loans (General Purpose Loans and Residential Loans for first-time home buyers) are available only to TSP participants who are in pay status and who contribute to the TSP through payroll deductions. A TSP participant repays both types of TSP loans (including interest charges) in regular payments. This is done either through payroll deductions if the TSP participant is federal service and in pay status, or by direct debit, check or money order after a TSP participant has separated from federal service.

A TSP participant who separates from federal service and who has an outstanding TSP loan has to decide if they want to immediately pay off the loan, keep the loan and set up monthly payments, or allow the TSP loan to be foreclosed and accept the fact that the outstanding balance and accrued interest is taxable with a 10 percent early penalty if the TSP participant is younger than age 59.5.

Advertisement

Failing to make TSP loan payments in accordance with a TSP participant Loan Promissory Note can have serious financial consequences. This is especially true if the TSP participant is still working or subject to an early withdrawal penalty tax. A TSP participant is responsible for ensuring that the TSP loan payments are correct and submitted on time regardless of whether the TSP participant’s agency missed the TSP participant’s payment.

For more information about TSP loans, TSP participants should go here.

Withdrawals and Distributions from a TSP Account

If a TSP participant separates from federal service before the year they become age 55, then the 10 percent IRS early withdrawal penalty will apply to most TSP withdrawals and all TSP loan distributions. A departed TSP participant has to wait until they are 59.5 in order to make penalty-free withdrawals.

Once a separated TSP participant becomes age 59.5, the participant has four options for making penalty-free TSP withdrawals:

(1) Partial distributions of a specified amount;

(2) Total distribution;

(3) Annuity purchase; and

(4) Installment payments.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019