Your high-3 average salary is one of the most important numbers used to calculate your Federal Employees Retirement System (FERS) pension. Despite its name, it is not simply your highest-paid three calendar years. Instead, it is the highest average basic pay you earned during any consecutive 36-month period of federal service.

Understanding how the high-3 is calculated can help you estimate your future pension, evaluate retirement timing, and avoid common misconceptions.

Key Takeaways

- The high-3 is the highest average rate of basic pay over any consecutive 36 months.

- It is based on basic pay, not your total compensation.

- Overtime, bonuses, awards, travel reimbursements, and most allowances are not included.

- Annual pay raises that occur during the 36-month period are reflected in the calculation.

- For most employees, the high-3 occurs during the final three years of federal service—but not always.

When federal employees begin planning for retirement, one of the first questions they ask is: “What is my high-3 average salary?”

The answer is important because your high-3 is one of the three primary factors used to determine your FERS basic annuity:

- Your high-3 average salary

- Your years and months of creditable service

- The FERS pension multiplier

Even a modest increase in your high-3 can increase your lifetime retirement income.

What Is the FERS High-3 Average Salary?

The Office of Personnel Management (OPM) defines the high-3 average salary as the highest average basic pay you earned during any consecutive 36 months of federal service.

Advertisement

Many employees mistakenly believe the high-3 refers to their highest-paid three calendar years. In reality, OPM looks for the highest-paid 36 consecutive months, regardless of where they fall during your federal career.

For example, your high-3 period could be:

- July 15, 2024 through July 14, 2027

- October 1, 2023 through September 30, 2026

The dates do not have to align with the beginning or end of a calendar year.

What Counts as Basic Pay?

Only basic pay is included in your high-3 calculation. This is important because many forms of compensation that increase your paycheck are not considered retirement-covered pay.

Basic pay generally includes:

- Base General Schedule (GS) salary

- Locality pay

- Special salary rates

- Law Enforcement Availability Pay (LEAP), when retirement deductions are withheld

- Administratively Uncontrollable Overtime (AUO), when retirement deductions apply

- Other forms of premium pay specifically designated as basic pay for retirement purposes

Basic pay generally does not include:

- Overtime pay

- Cash awards

- Performance bonuses

- Recruitment or relocation incentives

- Travel reimbursements

- Per diem

- Uniform allowances

- Moving expenses

- Most premium pay that is not subject to retirement deductions

As a result, your W-2 wages may be significantly higher than your official high-3 average salary.

How the High-3 Average Salary Is Calculated

OPM calculates your high-3 by identifying the consecutive 36-month period during which your average basic pay was the highest.

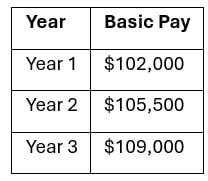

Suppose your annual basic pay was:

Your high-3 average would be:

($102,000 + $105,500 + $109,000) ÷ 3 = $105,500

In practice, OPM performs a more precise calculation because pay raises, promotions, and locality pay changes often occur during the middle of a year rather than on January 1.

Why Your High-3 Average Salary Matters

Your high-3 average salary is one of the three components used to calculate your FERS basic annuity.

For most employees, the formula is:

High-3 Average Salary × Years of Creditable Service × 1%

If you retire at age 62 or later with at least 20 years of creditable service, the multiplier generally increases to 1.1%, resulting in a larger pension.

Because the high-3 is multiplied by every year of service, even a relatively small increase can produce thousands of dollars in additional lifetime retirement income.

Example

Maria retires with:

- High-3 average salary: $120,000

- Creditable service: 30 years

- Standard FERS multiplier: 1%

Her annual FERS pension would be: $120,000 × 30 × 1% = $36,000 per year

If Maria qualified for the enhanced 1.1% multiplier by retiring at age 62 or older with at least 20 years of service, her annual pension would increase to:

$120,000 × 30 × 1.1% = $39,600 per year

That’s an increase of $3,600 annually before taxes.

Does Your High-3 Have to Be Your Last Three Years?

No. Although the final three years of federal employment are often the highest-paid because of annual pay raises and promotions, that is not always the case.

Your highest-paid consecutive 36 months could occur earlier if you:

- Accepted a lower-paying position before retirement

- Moved from a higher locality pay area to a lower one

- Left a position with a special salary rate

- Experienced a reduction in pay for another reason

OPM automatically identifies the consecutive 36-month period that produces the highest average basic pay.

Common Misconceptions

“It’s my highest three calendar years.”

No. The high-3 is based on 36 consecutive months, not calendar years.

“It includes overtime.”

Generally, no. Most overtime pay is excluded because it is not considered basic pay for retirement purposes.

“My W-2 salary is my high-3.”

Not necessarily. Your W-2 includes many forms of compensation that are excluded from the high-3 calculation.

“Working one more year always increases my high-3.”

Not always. If your earlier 36-month period already represents your highest average salary, working another year may not significantly change your high-3. However, another year of creditable service can still increase your pension.

Tips for Federal Employees

If you’re approaching retirement, consider these best practices:

- Review your SF-50s for accuracy.

- Verify that promotions and pay adjustments are correctly documented.

- Understand which types of pay count toward retirement.

- Estimate your FERS pension before selecting a retirement date.

- Remember that delaying retirement may increase both your years of service and your high-3 average salary.

Frequently Asked Questions

Does locality pay count toward my high-3?

Yes. Locality pay is generally considered part of your basic pay and is included in the calculation.

Do bonuses count toward my high-3?

No. Performance awards, cash awards, and bonuses are generally excluded.

Does overtime count toward my high-3?

Most overtime pay does not count because it is not considered basic pay for retirement purposes.

Can my high-3 come from the middle of my career?

Yes. OPM uses whichever consecutive 36-month period produces your highest average basic pay, regardless of when it occurred.

Who calculates my official high-3?

Your employing agency prepares your retirement records, and OPM makes the final determination when processing your retirement application.

Download the FERS High-3 Average Salary Estimator Worksheet

For educational purposes, you can download the free FERS High-3 Average Salary Estimator Worksheet (one page PDF).