Deagreez

Written by Sam Kovacs

Introduction

I learned a while ago that being too certain about anything in the stock market was the fastest and surest way to get humbled.

It happens too often. Investors are presented with a certain possible course of action, and they believe it is the only possible course of action. But you cannot pigeonhole your mind based on your personal preferences.

Which is why in October when everyone believed the market was doomed we asked: What if the 2022 bear market is already over?

We considered the possibility, and our take was that it was at least a lot more likely than the market was giving the outcome credit.

Price action since then suggests that it might very well have been the bottom.

Asking the question about what will happen in the short run can help you be prepared for all possible outcomes.

It can make the ups and downs of the market more tolerable.

But if you’re in this for the long haul, then whatever happens over the next year or two doesn’t really matter. Stocks will go up and down.

If you buy the right stocks at the right prices, you’ll come out on top.

This does bring up two questions: what are the right stocks, and what are the right prices?

Buying stocks at the right price.

The right price, for dividend investors like us, is the price which gives an investor a great yield given the stock’s dividend growth potential.

Sounds vague? Let’s break it down a little more.

It should be quite clear that there is a trade-off between yield and dividend growth.

The higher the dividend yield, the less you need that yield to grow, and vice versa.

It’s why some, like Chowder, tried to come up with ways of combining these two metrics. You’re probably familiar with the Chowder rule which just adds the yield to the growth rate. For example if a stock grows the dividend at 8% per annum and yields 3%, it has an 11% Chowder ratio.

It’s simple, but it’s highly ineffective.

It suggests that a 1% yielding stock growing its dividend at 11% per annum (12% Chowder) is the same as a 4% yielding stock growing its dividend at 8% per annum (also 12% Chowder).

Let’s pick a stock that yields 1% and a stock that yields 4% and project their income at these rates over ten years to prove the Chowder ratio wrong.

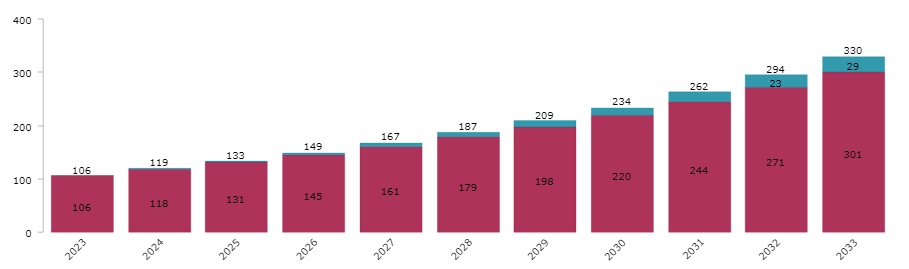

Let’s tike NIKE (NKE) which yields 1.12% and assume the dividend will grow at 11% per year for the next 10 years. This is conveniently in line with Nike’s 5 year dividend growth rate.

If we invest $10,000 in Nike today and forecast the income we’d receive from Nike over 10 years, assuming dividend reinvestments at a constant yield and 11% annual growth, then in year 10 you’d expect to receive $330 in annual income, of which $29 would have come from reinvesting dividends.

Nike Income Projection (Dividend Freedom Tribe)

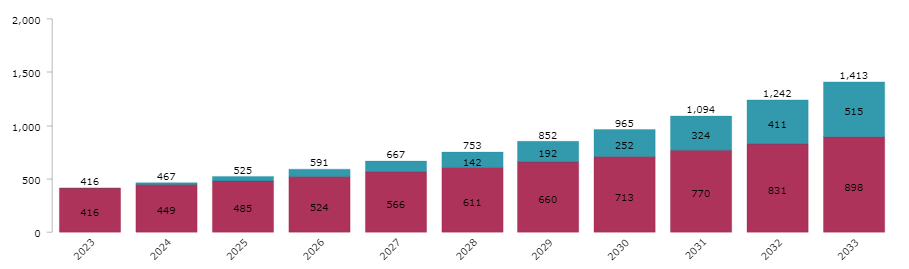

On the other hand, if we take a 4% yielding stock like Essex Property Trust (ESS) which yields 4.2%, and we project 8% dividend growth for the next decade (this is way above my personal projections for ESS, but please bear with me for the example).

If you invest $10K in ESS, and reinvest the dividends at a constant yield while the dividend grows at 8% per annum, then in year 10, you’d expect to receive $1,413 in income, of which $515 would have come from reinvesting dividends.

ESS Income Projection (Dividend Freedom Tribe)

So it is quite clear to me, as it should be to you, that $1,413 is a lot more than $330.

Heck, even if ESS didn’t grow its dividend at all, but you just reinvested the dividends (so a 4% Chowder), you’d still expect double the income in 10 years.

So Chowder doesn’t work. The reason it doesn’t work is that for every 1% decrease in yield, the increase in growth required goes up exponentially.

So over a 10 year horizon, while you might require a 5% growth rate for a 4% yield, you’ll require a 9% growth rate for a 3% yield, a 15% growth rate for a 2% yield, or a 25% growth rate for a 1% yield.

What’s better than Chowder?

Projecting 10 years out is better. Maybe you’d argue that projecting 20 years out is even better for some. However, we’ve found that taking a decade as our projected horizon to be very convenient.

Through experience and math, we’ve developed these rules of thumb ideal growth rates for different yields:

| Yield | Required Growth Rate |

| 2% | 13-15% |

| 3% | 9%-10% |

| 4% | 3.5-5% |

| 5% | 1-2% |

| 6% | 0-1% |

So, provided you find stocks with the ability to grow at the rates shown on the right with the yields on the left, you’ll be buying them at right prices.

But which ones are the right stocks?

Buying the right stocks

The right stocks to buy are the ones which are able to grow their business sufficiently and are sufficiently shareholder friendly to grow their dividend at the rate required to be a fruitful dividend investment.

The numbers above are useless if the companies don’t follow through.

Unlike earnings, dividends are harder to predict as they depend on the discretionary decisions of the board.

In 2022, when the market was down, many companies chose to increase their dividends by very small amounts, not because they couldn’t afford it, but because they didn’t believe the market would care.

Arbor Realty (ABR) was one such stock, and management were very transparent about this:

I think the Board in discussions and Paul can comment it on as well as, we just don’t get the credit in the market and at this period of time, there is really no upside in the market to raising the dividend. Everybody else is lowering their dividend. And the Board felt the credit is really — everybody’s dropping their dividend or paying it out of capital. And clearly the cushion we have and the thought was there is no real benefit to it.

The lesson: Growing dividends is not based just on the ability to increase but also on the willingness to do so.

The best proxy for a willingness to increase is a strong history of consistent dividend increases. Past increases are management’s “big stack of proof” that they care about shareholders.

So the right stocks are stocks which have proven that they are willing to increase their dividend.

Let’s not forget though, the ability to increase is also incredibly important.

You might be willing to go to the NBA, but if you’re unable to score a layup with your strong hand, your willingness won’t help much.

The ability to pay a dividend is determined by:

- A company’s cashflows

- Future growth of these cashflows.

Companies which can tick both boxes often have large moats, and are in industries which have secular tailwinds which make it “easy” for them to grow.

This is particularly important in the context of this article, which was titled stocks for “generational wealth”. A generation from now, we expect these stocks to have grown massively.

For that to happen, their end markets need to grow as well.

Here are 2 very high quality dividend stocks which you should consider buying today, which are all right stocks at the right price.

Buy Broadcom

Broadcom (AVGO) is one of my favorite stocks.

In an article last year, I made the case for semiconductors being the “$1 trillion opportunity”.

Essentially the argument was that over the next couple of decades, semiconductors will become ever more embedded into our economies: from the electrification of factories, the increase in the number of chips in cars to the deployment of wide scale network and broadband facilities.

Semiconductors are everywhere. And while the consumer oriented use cases (phones, laptops) will remain a cyclical consumer discretionary category, these other verticals are becoming less cyclical, as the secular growth reduces the downside variability which has usually been associated with the semiconductor industry.

Broadcom comes out as the cream of the crop. The fabless chip makers are exposed to all the right verticals for sustainable increased demand in the next few decades.

For a dividend investor, AVGO is a brilliant stock.

It pays 2.9%, still above its 10 year median yield of 2.6% while paying less than half of its FCF as a dividend.

AVGO DFT Chart (Dividend Freedom Tribe)

I believe the stock can continue to grow the dividend by 12-15% in upcoming years as it continues to see strong demand across all verticals.

AVGO is interestingly one of the better semiconductor companies, while at the same time being still mispriced. A fair price for AVGO would be when it yields anywhere between 2% and 2.5%, suggesting at least 15% upside from here.

I wouldn’t be surprised if 3 years from now, AVGO was a $1,000 stock.

In the years to come, Broadcom does face certain risks. While the semiconductor industry is becoming less cyclical, there will always be the usual ebbs and flows that impact demand. While Broadcom has extremely precise visibility into demand 12 months ahead, the market will price semiconductor stocks accordingly to general demand and this could hinder AVGO’s price action.

More fundamentally, supply chain disruption is always top of mind with semi’s. Broadcom is fabless, meaning it designs but doesn’t produce its chips. For instance, AVGO’s most recent 5G chip is produced by Taiwan Semiconductor (TSM). With Taiwan there is the oddball risk that China could invade Taiwan and severely disrupt the supply of semiconductors to the west. This would be a big blow to Broadcom.

Nonetheless, in my opinion these risks are just potential bumps in the road in a secular growth story, and not enough to justify avoiding AVGO.

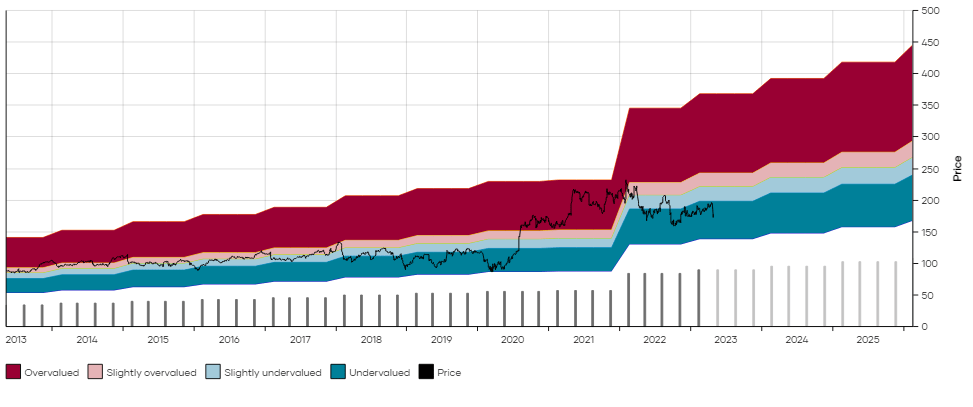

Buy UPS

United Parcel Service (UPS) currently trades at $173 and yields 3.74%, which is quite a bit more than its 10 year median yield of 2.93%.

UPS DFT Chart (Dividend Freedom Tribe)

The stock has been growing the dividend at a 10% CAGR during the past 10 years, but last year the growth rate was only 6.6%.

For a stock yielding 3.75%, 6-7% dividend growth is ideal.

The company pays out a reasonable 61% of free cashflow (or 48% of earnings).

I believe there are two clear long term trends which could benefit UPS and allow it to grow comfortably during the next decade.

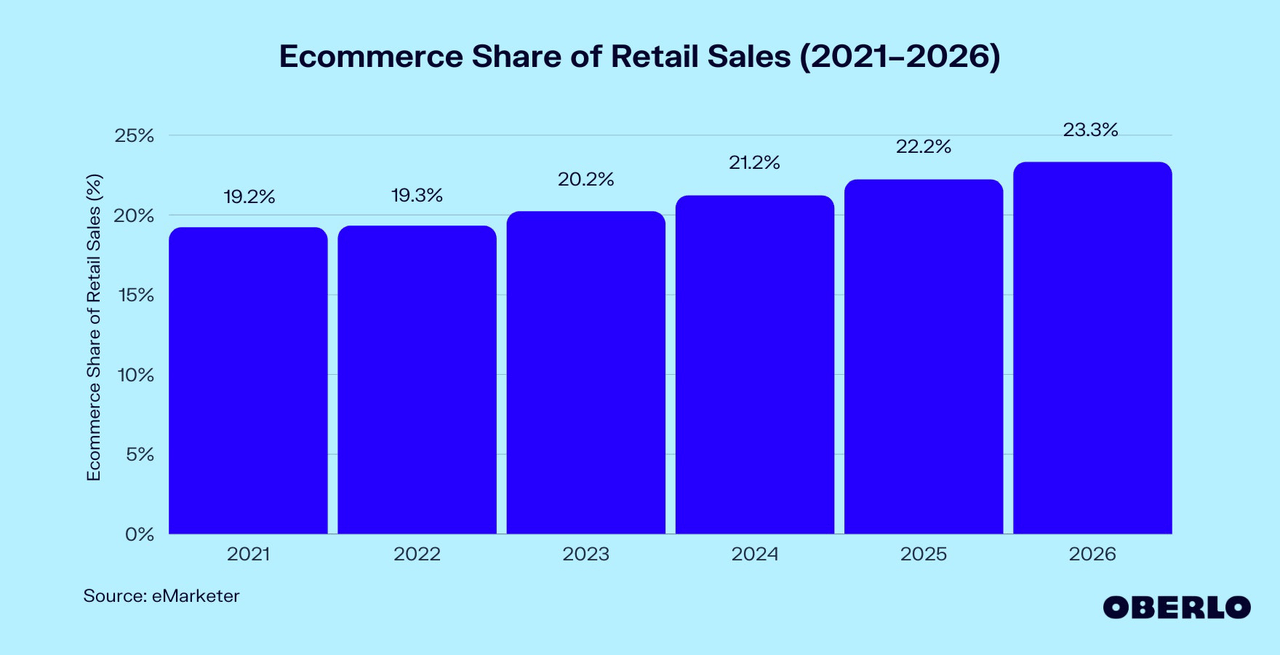

The first source of growth could come domestically from an increase in the market share of ecommerce in retail sales.

If you buy online, they’re going to send you a parcel. If they send you a parcel, there is a good chance that UPS is going to deliver it, as they have about 40% market share. FedEx (FDX) is the other major player (we are also long FDX but the stock is now on our watch/hold list)

As the share of ecommerce continues to climb throughout the next decade, there will naturally be more demand for UPS’ services.

eMarketer

How high can Ecommerce go as a percentage of retail sales? It is currently around 20%.

If we look at other countries, like South Korea for example, where the penetration rate of Ecommerce is already 35%, it is clear there is still room to grow.

This is a natural tailwind for the next decade.

The second big opportunity for UPS is internationally.

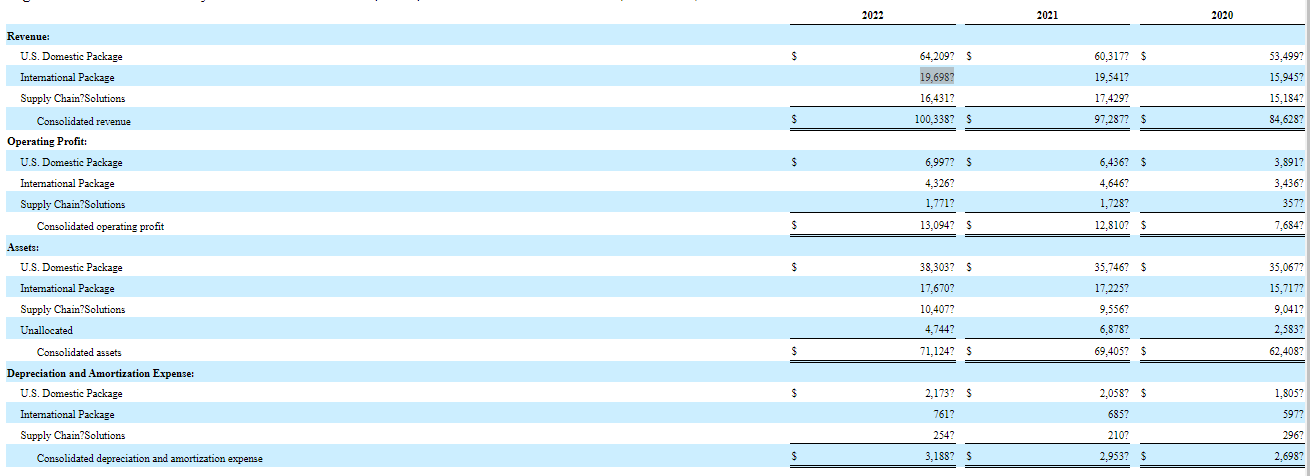

In 2022, UPS generated $64bn in revenue from US domestic packages, but only $19bn from international packages.

10K – Dividend Freedom Tribe

International expansion is a huge opportunity and is on management’s radar, as they continue to invest in their digital access program internationally, increasing the number of countries which can access the program to 16.

The digital access program allows small businesses to access deep UPS discounts at pre-negotiated rates through shipping software, which is an extremely valuable way to penetrate foreign markets.

For example, in China, SMEs contribute 68% of all exports. In India, small businesses account for 38% of the manufacturing output.

Needless to say, there is a lot of room for market growth for UPS.

Short term, retail package demand is tightly linked to consumer discretionary spending, which could cause some challenges to top and bottom line if the economy enters a recession.

This would be a temporary challenge for UPS, which could pull back its price.

It does not change the long term thesis, which is what truly matters when investing over a multi-year period.

Management runs a tight ship, and it is a business which I’m quite fond of. It is currently undervalued and makes a good investment.

Conclusion

Having a long time horizon is the biggest privilege amongst money managers who need to report quarter to quarter performance against the S&P 500.

If you can buy the really good stocks which have natural economic tailwinds, unless management fumbles, the stocks will naturally benefit over time.

Don’t optimize for next quarter. Optimize for a few years from now.

And get paid a growing dividend to wait.