Intel (INTC) is expected to announce its Q3 earnings report later this week, and unlike the last few times, there is visibly more optimism among investors. It is not difficult to figure out why. The quarter began with Trump doubling down on Intel’s CEO Lip-Bu Tan, based on his ties to the Chinese military through some past investments. One in-person meeting with the CEO resolved all the doubts, and less than two weeks after that, the U.S. government took a 10% stake in the struggling chipmaker. The share price closed that day at $24.80.

As we approach the Q3 earnings, the stock is already up well over 50% since that announcement. The company has made a visible shift. It brought in some new people at the beginning of September, and there is one thing in common among them: they all come from an engineering role at their previous employer. Investors may think that’s obvious for a chipmaker and not a big deal, but a little background story should help understand the context.

Arguably, Intel’s decline started in 2005 when Paul Otellini became the first “non-engineer” CEO of the company. He was an economics graduate, and Intel shifted its focus from innovation to business, as it was the technology leader for years anyway. Years later, Intel lost the technology lead, and the ongoing efforts to reclaim that lead are all about bringing innovation to the core of Intel. These appointments were followed by the announcement of a $5 billion investment in INTC stock by Nvidia (NVDA). Prior to that, SoftBank (SFTBY) had also announced a $2 billion investment. Investors finally recognized the shift, and the stock reacted accordingly.

It will take some time for these developments to turn into profits, but there’s an expectation that this quarter will bring in better-than-expected results. Intel now has the backing of the U.S. government and investors. The new backing will be leveraged to attract customers for the 18A node while carefully allocating resources for the development of Intel 14A. From here on, it all depends on Intel’s engineering expertise. The numbers will take care of themselves once that happens. Investors should expect a positive earnings surprise, but that is only the beginning of the turnaround story.

Intel, commonly known as the chipmaker powering an everyday user’s PC or laptop, is a designer and manufacturer of computing equipment. It is headquartered in Santa Clara, United States, and despite recent struggles, continues to dominate the PC market through its CPUs.

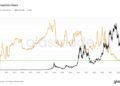

INTC stock has surged over 89% on a year-to-date (YTD) basis, outperforming the Nasdaq Composite’s ($NASX) 17.45% by a huge margin. Currently, the stock is trading at an approximate 28% discount to its 3-year high of $51.28.

www.barchart.com

With such a noticeable jump in share price this year, INTC looks to have run its course at first sight. However, the stock is still trading at a forward price-to-sales (P/S) multiple of 3.38x, which is around 3% below the sector median of 3.49x. With a forward price-to-book (P/B) multiple of 1.52x, the stock is trading at a larger discount of 66% to the sector median and a 6% discount to its own 5-year average P/B ratio. Hence, one can clearly see further upside potential from here.

Intel announced its second-quarter earnings on July 24. The company’s revenues were flat year-on-year (YoY), standing at $12.9 billion and handily beating the estimates by $977.2 million. However, the GAAP EPS was recorded at -$0.67, missing the analyst consensus by $0.39. Key drivers of losses include $1.9 billion of restructuring charges and $800 million of non-cash impairment charges. During the quarter, the company also incurred $200 million of one-time charges that had a -$0.23 impact on GAAP EPS.

With a focus on core products and an AI roadmap, backed by workforce reduction and improved capital efficiency, the company aims to streamline business operations and optimize the balance sheet. Management has provided third-quarter revenue guidance between $12.6 billion and $13.6 billion. As per estimates, the midpoint will lead to gross margins around 36% and an anticipated EPS of -$0.24 for the quarter. The consensus is that these estimates will be comfortably beaten, and the company may even post a profit. However, the earnings on Oct. 23 will contain important announcements related to Intel’s 18A and 14A plans. As previously stated, the numbers might be of interest to swing traders for now, but the earnings will be all about Intel’s product roadmap.

Analysts are predominantly negative on Intel, not surprising considering the company’s struggles in the past two years. Of the 41 analysts who cover the stock, only two have a “Strong Buy” rating, with a whopping 33 calling the company a “Hold.” The remaining six are divided between five “Strong Sell” and one “Moderate Sell” ratings.

The mean target price on the stock is $27.77, and the stock was trading above this level even after its one-month rally of 32%. The highest target price stands at $43, fetching an upside of 13%. Considering the recent events and a potentially positive earnings call, one can expect these target prices to nudge upwards as analysts digest the leadership shift and changing financial dynamics of the company.

www.barchart.com

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. This article was originally published on Barchart.com

Trades High School Partnership DirectorSpokane CollegesLocation: Spokane CC Main Campus SpokaneDepartment: SCC VP of Instruction OfficeSalary Range:...