Federal employees spend years building a clear picture of their retirement income. Far less attention is given to how state taxes will affect what that income looks like in practice. While relocating to a different state is often a goal in retirement, knowing how each location will impact your money can make a huge difference.

Most people hear about the nine states with no income tax and assume the decision is simple. It is not. The real picture is more detailed, and it opens the door to planning opportunities that go beyond choosing where to live.

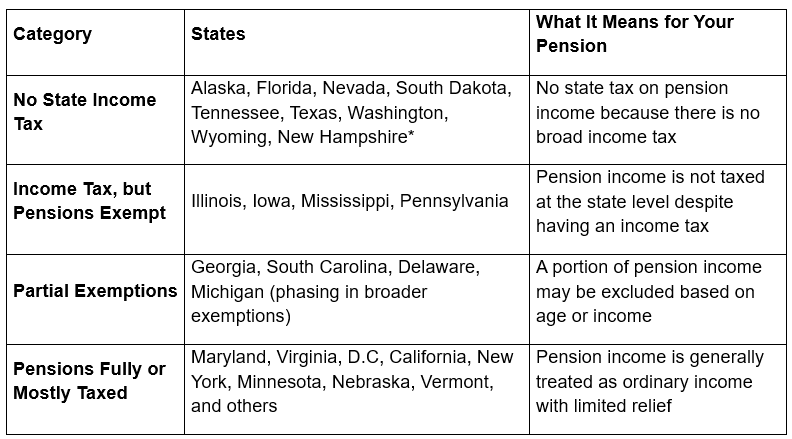

State tax treatment is inconsistent

At the federal level, pension income is taxable. At the state level, there is no consistent rule. Some states have no income tax at all. Others tax income but exclude retirement income. A third group taxes pension income in full or with only limited relief.

States such as Illinois, Iowa, Mississippi, and Pennsylvania fall into the second category. They tax income generally but exclude most retirement income, including pensions and, in many cases, withdrawals from retirement accounts.

Then there are states like California, New York, Minnesota, and Vermont. These states tax pension income as ordinary income, with fewer exemptions than many retirees expect.

Between those groups are states that offer partial relief. Georgia, South Carolina, and Delaware allow exclusions based on age or income. Michigan is in the process of expanding its exemptions, with broader relief taking effect over the next few years.

For current and former federal employees, these differences matter. Pension income from FERS or CSRS does not receive special treatment in most states. It is simply income, and how it is taxed depends on where you live.

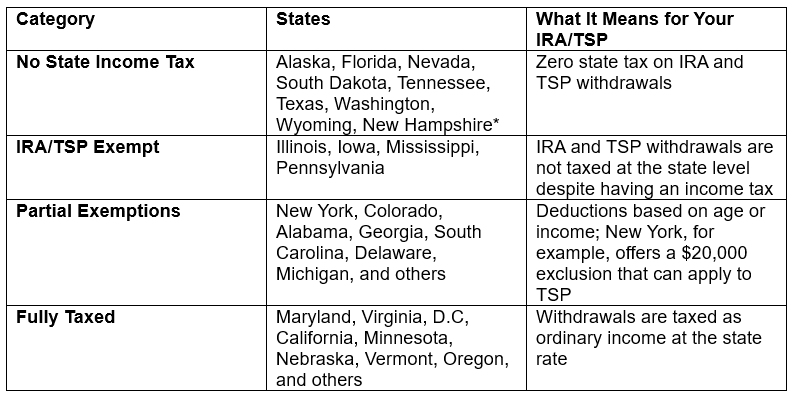

Traditional IRA and TSP withdrawals follow the same pattern

Traditional IRA and TSP distributions are taxed as ordinary income at the federal level. At the state level, the treatment generally tracks the same four-tier pattern as pensions, but the specifics are not identical. A state that exempts pensions does not automatically exempt IRA or TSP withdrawals, and vice versa.

Advertisement

For federal employees, the takeaway is that pension treatment and TSP/IRA treatment must be checked separately when evaluating a state. The two streams can land in different tiers.

Moving is not a complete answer

It is common to frame this decision as a relocation question. Should you move to a state with no income tax? That question misses the larger issue.

A state with no income tax may have higher property taxes, higher insurance costs, or a higher cost of living. A state that taxes pension income may still produce a lower overall cost depending on your situation. Contrary to what most believe, taxes in retirement are not driven by location alone, but how income is structured and when it is taken. Two retirees in the same state can have very different tax outcomes based on their withdrawal strategy.

Income sequencing changes the outcome

Retirement income is not a single stream. It is a mix of sources, each treated differently for tax purposes.

• Pension income may be fully taxable at the state level.

• Social Security is exempt in most states.

• Roth withdrawals are generally tax-free.

• Traditional TSP and IRA withdrawals are usually taxable.

This creates flexibility and the need for a more comprehensive view of possible outcomes.

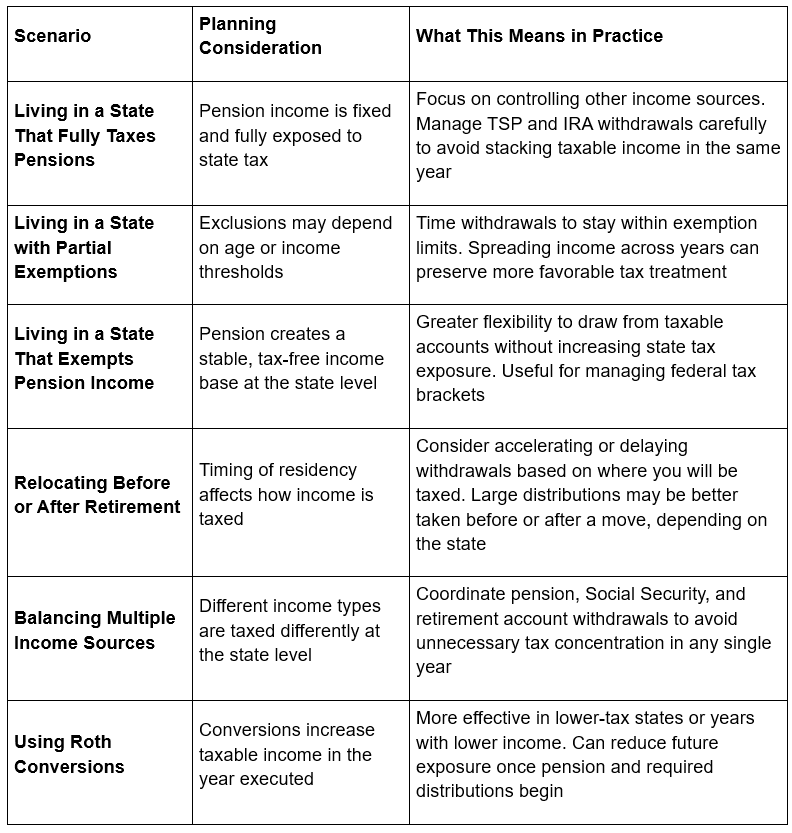

A retiree who draws heavily from taxable sources in one year may push themselves into higher state tax exposure. Another retiree who balances withdrawals across accounts may reduce that exposure. This is an example of where planning is put into practice.

Decisions such as when to begin withdrawals, how much to take from each account, and whether to convert assets to Roth accounts can influence how much income is exposed to state taxes over time. These are not one-time decisions, but various ones which need to be evaluated across multiple years.

Coordination matters more than most expect

Tax planning is one area where disconnected advice creates problems. A financial plan that does not account for state taxes can overstate how long assets will last. A tax return prepared without forward-looking planning can miss opportunities to reduce future tax exposure.

Federal employees often have three primary income sources in retirement: a pension, the TSP, and Social Security. The pension offers little flexibility. The TSP and other retirement accounts do. That flexibility is where planning has the most impact.

When financial planning and tax preparation are coordinated, it becomes possible to look beyond a single tax year. Income can be timed. Withdrawals can be adjusted and future tax exposure can be managed with more precision.

This approach relies on projecting income across multiple years and adjusting before decisions become fixed. Once those variables are clear, the focus shifts from rules to decisions:

The better question to ask

The question more people should be asking is how location and income strategy work together.

For some retirees, relocating to a state with no income tax makes sense. For others, the benefit is smaller once other costs are considered. In many cases, the strongest outcome comes from a combination of location decisions and disciplined income planning. State tax rules offer flexibility and can be actively managed rather than being simply overlooked.

Decisions have practical implications

Federal employees enter retirement with a level of structure that many private-sector workers do not have. That structure creates stability, but it also creates fixed income streams that are harder to adjust. Because of that, the decisions that remain flexible carry more weight.

Where you live is one, but how you draw income is another. Handled carefully and collaboratively, these decisions can reduce unnecessary tax exposure and extend your retirement income.

The variations between states go beyond differences in weather and the presence or absence of state income taxes. These strategies take both taxes and income into account together, instead of dealing with them individually.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

This information is not intended to be a substitute for individualized tax advice. We suggest that you discuss your specific tax situation with a qualified tax advisor.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA.

About the Author

Neil Cain is a certified financial planner with Capital Financial Planners. If you don’t feel confident in your current or future retirement withdrawal strategy and would like feedback, you can register for a complimentary Retirement Readiness Meeting. For topics covered in even greater depth, see our YouTube page.